The 18-week pre-laying period is the only phase of a layer production cycle where costs run continuously, and revenue is zero. Every other challenge in layer farming — disease, heat stress, poor FCR, market access — occurs while the farm is at least generating some egg income to offset costs. The rearing period does not. For 126 days, the farm consumes feed, pays labor, runs utilities, administers vaccines, and produces nothing that can be sold.

This is why more first-cycle layer farms fail during rearing than at any other point in the production cycle. Not because rearing is technically difficult. Not because disease events are more severe during rearing than during lay. But because the farmer who invested their available capital in infrastructure arrived at week 6 with birds that are consuming 65 kg of feed per day, and a bank account that cannot cover the next feed delivery.

The farms that survive the rearing period and arrive at the point of lay with healthy, uniform birds and a solvent balance sheet are not the farms with the most capital. They are the farms whose farmers planned the cash outflow schedule before spending a franc on construction — and built their financial position to match the plan.

This article builds that plan: a weekly cash outflow model for the 18-week rearing period, the reserve calculations that determine how much liquid capital is needed before day one, the supplier credit strategies that extend the runway, and the operational decisions that reduce cash burn without compromising bird performance.

The Rearing Period Financial Reality: What Happens Week by Week

Before building the financial model, understand the biology driving the cash requirement. Rearing cost is not linear — it rises progressively as birds grow and their feed intake increases.

Feed Intake Progression During Rearing

Feed consumption is the largest cash cost driver and the one that changes most week by week:

| Age (Weeks) | Daily Feed Per Bird (g) | Daily Feed for 1,000 Birds (kg) | Daily Feed Cost (XAF at 300/kg) |

|---|---|---|---|

| 1–2 | 15–25 | 15–25 | 4,500–7,500 |

| 3–4 | 30–40 | 30–40 | 9,000–12,000 |

| 5–6 | 45–55 | 45–55 | 13,500–16,500 |

| 7–8 | 60–70 | 60–70 | 18,000–21,000 |

| 9–10 | 70–80 | 70–80 | 21,000–24,000 |

| 11–12 | 80–88 | 80–88 | 24,000–26,400 |

| 13–14 | 90–96 | 90–96 | 27,000–28,800 |

| 15–16 | 96–100 | 96–100 | 28,800–30,000 |

| 17–18 | 100–105 | 100–105 | 30,000–31,500 |

Total rearing feed consumption for 1,000 birds (18 weeks): approximately 6,200–6,500 kg

Total feed cost at XAF 300/kg: approximately XAF 1,860,000–1,950,000

By week 14, the farm is spending approximately XAF 27,000–29,000 per day on feed alone. Add labor (XAF 1,500–2,500/day), utilities (XAF 1,000–1,500/day), and weekly health inputs (amortized to approximately XAF 2,000–3,000/day), and the total daily cash burn in the final weeks of rearing reaches XAF 32,000–36,000 per day with zero revenue to offset it.

The Complete 18-Week Cash Flow Model

The following model tracks cumulative cash outflows for a 1,000-bird layer farm from day 1 through week 18 at first egg.

One-Time Costs at or Before Placement

These costs occur before or at the time of chick arrival and must be fully funded from reserves:

| Item | Amount (XAF) |

|---|---|

| Day-old chicks (1,050 purchased) | 1,260,000 |

| Disinfection and house preparation | 80,000 |

| First 2 weeks’ feed supply (pre-stocked) | 90,000 |

| Initial brooding supplies and equipment checks | 45,000 |

| Total pre-placement costs | 1,475,000 |

Weekly Cash Outflows — Weeks 1–18

| Week | Feed (XAF) | Health Inputs (XAF) | Labor (XAF) | Utilities (XAF) | Total Weekly (XAF) | Cumulative (XAF) |

|---|---|---|---|---|---|---|

| 1–2 | 87,500 | 85,000 (vaccines + brooding) | 25,000 | 15,000 | 212,500 | 1,687,500 |

| 3–4 | 140,000 | 20,000 | 25,000 | 15,000 | 200,000 | 1,887,500 |

| 5–6 | 175,000 | 35,000 (Fowl Pox + boosters) | 25,000 | 15,000 | 250,000 | 2,137,500 |

| 7–8 | 224,000 | 15,000 | 25,000 | 15,000 | 279,000 | 2,416,500 |

| 9–10 | 259,000 | 15,000 | 25,000 | 15,000 | 314,000 | 2,730,500 |

| 11–12 | 300,000 | 25,000 (Coryza dose 1) | 25,000 | 15,000 | 365,000 | 3,095,500 |

| 13–14 | 322,000 | 35,000 (IB vaccine + Coryza dose 2) | 25,000 | 15,000 | 397,000 | 3,492,500 |

| 15–16 | 336,000 | 15,000 | 25,000 | 15,000 | 391,000 | 3,883,500 |

| 17–18 | 350,000 | 80,000 (killed ND+IB+EDS pre-transfer) | 25,000 | 15,000 | 470,000 | 4,353,500 |

Total cumulative cash outflow through week 18: approximately XAF 4,353,500

This is the minimum liquid capital required to sustain a 1,000-bird flock through the rearing period — before any egg revenue is received. A farm that begins the rearing period with less than XAF 4.5 million in liquid funds (after CAPEX has been spent on infrastructure) will run out of feed money before the first egg is laid.

The Reserve Calculation: How Much Liquid Capital You Actually Need

The cumulative cash model above provides the minimum rearing period capital requirement. The reserve calculation adds a buffer for three realities that the model assumes away:

Reality 1 — Feed price volatility: Feed prices in West Africa have increased 25–40% between 2022 and 2025. A 10% increase above the XAF 300/kg model assumption adds approximately XAF 186,000 to the total rearing feed cost. The reserve must absorb this without triggering a cash shortfall.

Reality 2 — Disease treatment events: A single antibiotic treatment course during rearing costs XAF 40,000–90,000. The model includes routine vaccination but not emergency treatment. Allow for 1–2 unplanned treatment events.

Reality 3 — Payment timing mismatches: Feed must typically be paid for at delivery or within 7 days. Utility bills arrive monthly. Wage payments are weekly or monthly. The cash reserve must be large enough to cover payments when they fall due, not when the annual cash flow model shows them as affordable.

The Reserve Formula

Required Liquid Reserve = Cumulative Cash Outflow (18 weeks) + Price Volatility Buffer + Emergency Treatment Buffer + Payment Timing Buffer

= XAF 4,353,500 + XAF 200,000 + XAF 100,000 + XAF 350,000

= XAF 5,003,500 minimum liquid reserve at time of chick placement

In practice, round up to XAF 5.0–5.5 million as the liquid capital target for the rearing period. This is the amount that must be held in accessible form — cash, bank account, confirmed credit line — separate from and in addition to the CAPEX already spent on infrastructure.

A farm with CAPEX of XAF 8.5 million and rearing reserve of XAF 5.0 million requires XAF 13.5 million in total startup capital — consistent with the XAF 11.5–14 million range calculated in the cost analysis article, with the difference driven by market location and construction specification.

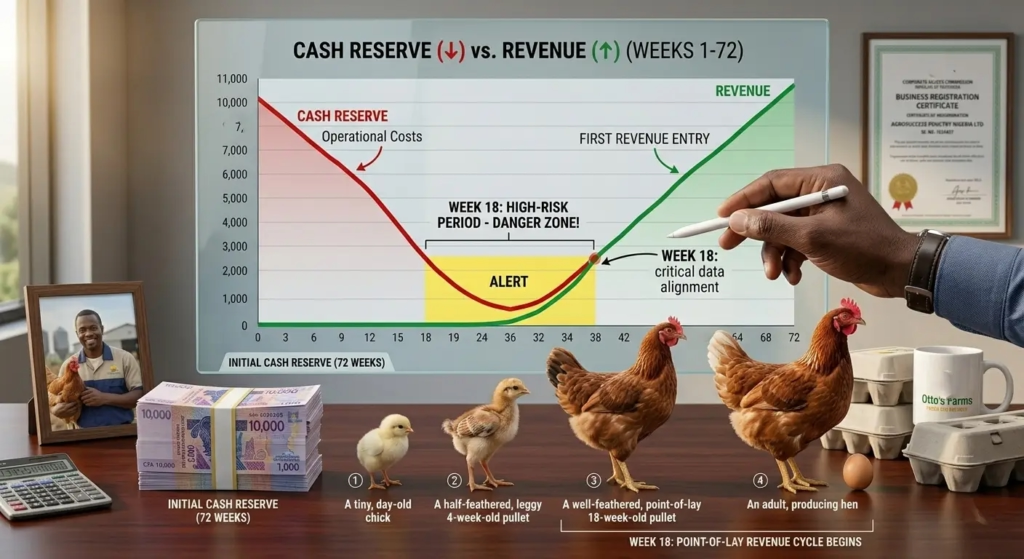

The First Egg Revenue Bridge: Weeks 18–24

The first egg revenue does not immediately replace the cash outflow. There is a transition period — approximately weeks 18–24 — during which laying rate is ramping up from 5% to 50–60% and daily revenue is building toward the level that covers daily costs.

The Revenue Ramp-Up Model

| Week of Lay | Approx. Laying Rate | Daily Eggs (950 hens) | Daily Revenue at XAF 140 | Daily Costs | Daily Net Cash Flow |

|---|---|---|---|---|---|

| Week 1 of lay (wk 18) | 5–10% | 48–95 | 6,720–13,300 | 50,000 | −43,280 to −36,700 |

| Week 2 of lay (wk 19) | 15–25% | 143–238 | 20,020–33,320 | 50,000 | −29,980 to −16,680 |

| Week 3 of lay (wk 20) | 30–45% | 285–428 | 39,900–59,920 | 50,000 | −10,100 to +9,920 |

| Week 4 of lay (wk 21) | 50–65% | 475–618 | 66,500–86,520 | 52,000 | +14,500 to +34,520 |

| Week 5 of lay (wk 22) | 70–80% | 665–760 | 93,100–106,400 | 52,000 | +41,100 to +54,400 |

| Week 6 of lay (wk 23) | 80–90% | 760–855 | 106,400–119,700 | 53,000 | +53,400 to +66,700 |

Key insight: The farm does not become cash-flow positive until approximately week 3–4 of lay (weeks 20–21 of the cycle). For the first three weeks of laying production — weeks 18–20 — the farm is still in a net cash deficit, spending more per day than eggs are generating.

This transition period requires an additional XAF 500,000–900,000 in reserve beyond the rearing period model to bridge the final negative cash flow weeks between rearing completion and self-sustaining positive cash flow.

Total reserve including transition bridge: XAF 5.5–6.0 million

This is the figure that should be in the bank before the first chick arrives — separate from CAPEX that has already been spent on the infrastructure.

Supplier Credit Strategies: Extending the Cash Runway

Not all rearing period costs must be paid from reserves at the moment they are incurred. Supplier credit — negotiated payment terms with feed mills, veterinary suppliers, and other input providers — can reduce the peak liquid capital requirement by extending payment timing without reducing consumption.

Feed Mill Credit

Feed is the largest rearing period cash cost. A credit arrangement with the feed mill that allows 14–21 days of payment deferral on each delivery reduces the peak liquid requirement by approximately XAF 500,000–800,000 at 14 days or XAF 750,000–1,200,000 at 21 days.

How to negotiate feed mill credit for a first-cycle operation:

- Approach the mill before chick placement — not during rearing when cash pressure is evident. Requesting credit from a position of need is a weaker negotiating position than requesting it as a business planning discussion before production begins.

- Offer a personal guarantee or collateral (land title, equipment) as security for the credit line

- Propose a structured repayment schedule starting from the first egg revenue — mills that understand the production cycle are often willing to structure credit around this timeline

- Start with a smaller credit amount (XAF 500,000) and demonstrate reliable repayment for the first cycle before requesting a larger facility in cycle 2

Not all mills will extend credit to first-cycle operations. Where credit is not available, consider paying 4–6 weeks of feed in advance at negotiated bulk pricing — this reduces per-kg cost by 2–5% while ensuring feed supply continuity without weekly payment pressure.

Veterinary Supplier Credit

Vaccine suppliers and veterinary product distributors often extend 30–60 day payment terms on scheduled vaccination programs for established customers. For a first-cycle operation, request payment on delivery for the first 2–3 vaccine orders and use that history to establish a 30-day credit facility from week 6 onward.

Labor Payment Timing

If employing one full-time farmhand, negotiate a bimonthly payment schedule (twice per month) rather than weekly payments. This reduces the weekly cash flow peaks associated with wage payment and allows the reserve to cover 2 weeks of accumulated wage payments rather than requiring weekly disbursement. Ensure the employment arrangement is clearly documented, regardless of the payment schedule.

Utility Pre-Payment vs. Credit

Electricity and water utilities in Cameroon and Nigeria typically require prepayment (prepaid meter systems) or payment on a monthly basis. There is limited scope for credit negotiation. Instead, optimize consumption:

- Use natural ventilation during the day and run fans only during peak heat hours to minimize electricity consumption during rearing

- Fix all water line leaks immediately — a dripping nipple wasting 1 liter per hour costs less in water than in the labor and management distraction of wet litter management, but all leakage is waste

Operational Decisions That Reduce Cash Burn Without Sacrificing Performance

Cash reserve management during rearing is not only about having enough money in the bank. It is also about spending that money efficiently — reducing costs that do not contribute to bird performance while protecting spending on inputs that directly determine the quality of the flock that arrives at the laying house.

Where to Reduce Spending

Reduce: Heating costs during brooding. In West African tropical climates, the ambient temperature during brooding (typically 28–35°C) means that supplemental heat is only needed during night hours and early mornings — not for 24 hours. Turn off brooders when the house temperature exceeds 31°C at chick level. A brooder running all day in a house that is already at 32°C ambient is consuming fuel without benefit and creating a thermal stress risk.

Reduce: Over-vaccination. The vaccination schedule in the vaccination article is the correct minimum program. Adding extra vaccination events — particularly repeat doses of vaccines already correctly administered — consumes budget without improving immunity in a correctly vaccinated flock. Run the scheduled program. Do not add events because “more is better.”

Reduce: Antibiotic prophylaxis. Routinely treating healthy birds with antibiotics as a “preventive” measure consumes health budget, increases resistance risk, and does not improve production performance in a biosecurity-managed flock. Reserve antibiotic expenditure for confirmed treatment indications.

Where Not to Reduce Spending

Do not reduce: Feed quantity. Underfeeding during the rearing period produces below-target body weight at point of lay, poor flock uniformity, and a compressed first-cycle production curve that costs far more in lost revenue than the feed cost saved. If cash pressure forces a choice between reducing feed quantity and reducing another cost, protect feed quantity.

Do not reduce: Vaccine quality. Substituting a lower-cost vaccine from an unreliable cold chain for the correct product saves XAF 15,000–30,000. A Newcastle outbreak from vaccine failure costs XAF 3–5 million in mortality, production loss, and replacement. This is not a cost reduction. It is a risk transfer from a known small cost to a probable large one.

Do not reduce: Body weight monitoring. Weekly weighing and flock uniformity assessment requires 1–2 hours of labor per week. It is the earliest warning system for the nutritional and management problems that, if undetected until week 15, cannot be corrected before the point of lay. The feed already consumed to produce an underweight flock is gone. The investment to weigh and detect the problem early is trivial.

The Pre-Laying Period Cash Flow Dashboard

A cash flow dashboard for the rearing period is not a complex financial model. It is a simple weekly tracking tool that answers three questions every Sunday:

- How much cash did I spend this week? — Total of all payments made: feed, labor, health inputs, utilities, consumables

- How much cash do I have remaining? — Bank balance + cash on hand − outstanding payment obligations due this week

- Am I on track? — Compare remaining cash against the cumulative outflow schedule. If actual cash remaining is less than the projected remaining reserve by more than 10%, investigate the deviation: was there an unplanned expense? Is feed consumption higher than modelled? Is a supplier charging above the agreed rate?

This weekly dashboard takes 15 minutes to complete. It converts a 5.0–5.5 million franc reserve into a managed resource — tracked against a plan — rather than a fund that depletes with each expense until it is exhausted without warning.

The Dashboard Template

| Item | Week ___ | Week ___ | Week ___ |

|---|---|---|---|

| Feed payment (XAF) | |||

| Labor payment (XAF) | |||

| Health inputs payment (XAF) | |||

| Utilities payment (XAF) | |||

| Other expenses (XAF) | |||

| Total this week | |||

| Cumulative spending | |||

| Cash remaining | |||

| Projected remaining (model) | |||

| Variance (actual vs. model) | |||

| Note any significant variances |

Fill this in weekly — not monthly, not “when needed.” A monthly review during the rearing period is too infrequent to catch a cash shortfall before it becomes a feed payment crisis.

What to Do If You Discover a Cash Shortfall Mid-Rearing

Even with correct planning, unexpected events create cash shortfalls during rearing: a disease treatment event, a feed price spike, equipment failure requiring repair, or the chick mortality rate exceeding the planned 5% buffer.

If the weekly dashboard shows a projected shortfall in the next 3–4 weeks, the response options in order of preference are:

Option 1 — Accelerate egg pre-sales. Some buyers — particularly restaurants and hotels — will pre-purchase eggs at a slightly discounted price in exchange for guaranteed supply from week 22 onward. A pre-sale of XAF 500,000–1,000,000 of future production at a 5–10% discount provides immediate cash inflow that bridges the shortfall without interest costs.

Option 2 — Negotiate short-term feed credit. Contact the feed mill supplier with a specific request: “I need 4 weeks of payment deferral to bridge a temporary shortfall. My first eggs are at week 18 and I will begin repayment at week 20 from egg revenue.” Most mills prefer a managed deferral request to an unpaid invoice that arrives without warning.

Option 3 — Reduce non-essential discretionary spending. Review the coming weeks’ planned expenditures. Are there any expenses that can be deferred without affecting bird health? Cosmetic farm maintenance, additional equipment purchases, supplemental products beyond the core program — defer these until first egg revenue begins.

Option 4 — Bring in a short-term financial partner. A family member, cooperative member, or agricultural microfinance institution providing a short-term cash injection against the specific security of confirmed first-egg production can bridge a gap of XAF 300,000–700,000. This is a better option than reducing feed quantity, which has permanent consequences on the flock that enters the laying house.

Option 5 — Reduce feed quantity as a last resort. Reducing feed allocation by 10% for 2–3 weeks saves approximately XAF 60,000–80,000 per week. This should only be considered as a last resort and only for birds in weeks 7–14, where controlled feeding is part of the grower phase protocol anyway. Never reduce starter feed below the requirement in weeks 1–6 — the gut development and skeletal growth damage is permanent. Never restrict pre-lay ration in weeks 15–18 — the calcium loading and reproductive preparation damage carries into the laying cycle.

Planning for the Second Cycle: Building Financial Resilience

The first rearing cycle is the most cash-constrained because there is no cash cushion from prior production. By the end of the first cycle, if the farm has been profitable, the cumulative net profit provides the working capital reserve for the second cycle’s rearing period — potentially without any additional external capital.

The target financial position at the end of the first cycle:

- Second cycle’s rearing period reserve (XAF 5.0–5.5M) held in the operating account before the cleanout begins

- CAPEX maintenance fund (XAF 500,000–800,000) for any repairs, cage replacements, or equipment maintenance identified during depopulation

- Owner profit distribution — whatever remains after the two above reserves are funded

A farm that depopulates the first cycle and immediately distributes all net profit to the owner before confirming the second cycle’s rearing reserve is funded has the same cash flow problem in cycle 2 as it had in cycle 1. The discipline of holding the rearing reserve before profit distribution is the financial habit that converts a first-cycle survivor into a multi-cycle sustainable operation.

Summary

The 18-week pre-laying period is not a waiting room before the farm becomes a business. It is the most capital-intensive phase of the production cycle — one that consumes XAF 4.3–4.4 million before the first egg is laid, requires an additional XAF 500,000–900,000 to bridge the production ramp-up period, and demands weekly cash flow monitoring from day one to prevent a feed payment crisis from destroying a flock that was otherwise being managed correctly.

The farms that manage this period successfully are not the richest farms at the start of the cycle. They are the farms whose farmers calculated the weekly cash outflow schedule before spending a franc on construction, built the reserve to match the schedule, negotiated the supplier relationships that extend the runway, tracked spending weekly against the model, and responded to emerging shortfalls with a structured plan rather than a feed reduction that compromises the birds.

The rearing period is where layer farm businesses are won or lost — not at disease events or market disruptions, but at the feed payment desk in week 8. Know how much you will spend. Know when you will spend it. Keep the money there to spend it.

The first egg is 18 weeks away. The planning starts today.

Download the analysis in PDF: Ottos_Farms_18Week_Financial_Plan.pdf